Problems created by end-of-quarter discounts are typical examples of the downside of focusing on local goals (in this case, sales targets). Although such actions can undermine the whole system, they take place in companies again and again.

Discounting Discounts

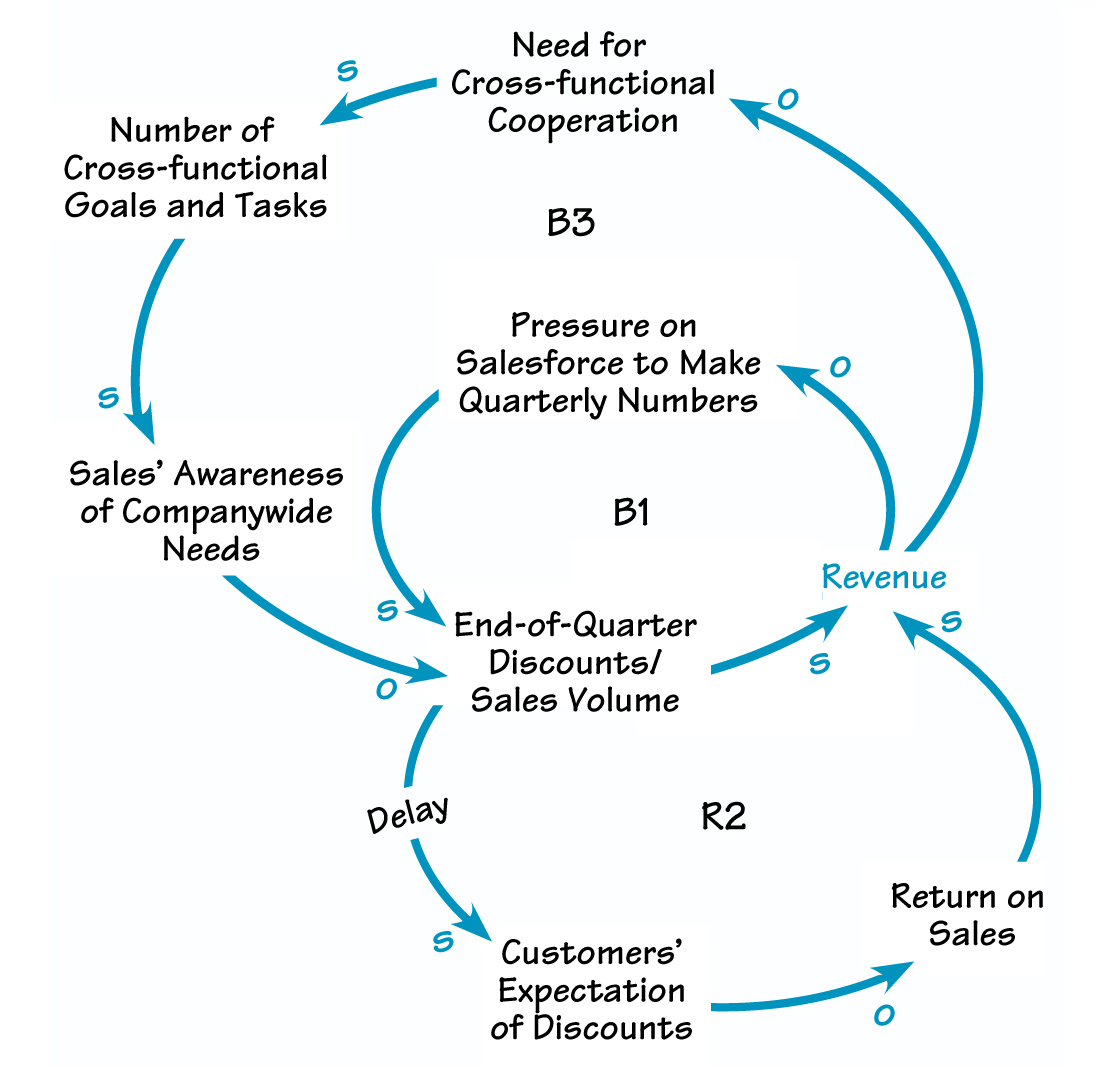

When reading the loops, note that R2 includes the variables in B1, and B3 includes the variables in R2.

Salespeople typically have a strong “win” mentality; it does not matter whether they are the sales chief, an area manager, or a sales rep. With little exaggeration, we can say that if they do not win, they do not exist. This “I need to win; I want to be the best” mindset is often valuable for initiating progress, new ideas, growth, and creativity. Therefore, management’s task is to understand and intentionally leverage this mentality for the benefit of the whole system, and not just that of the individual or the sales department. I frequently observe situations in which people behave competitively, although they do not want to and are sure they do not do so. Two things can help for using this natural human tendency: First, I must clearly define with what and whom I can compete without undermining the company’s viability, and second, I must determine who my teammates and colleagues really are. To that end, sales people need more information about the consequences of their actions on other departments—and on the entire organization.

Company vision and values are not enough to support cross-functional teamwork. Managers should work on establishing systems and procedures for initiating collaboration and information exchange between sales and other departments. But merely holding formal meetings is not enough; when people truly collaborate, they have common goals and tasks. What these common tasks could be depends on the company’s products and services, its market and its position in this market, and other features.

As a company’s revenue falls, its need for cross-functional cooperation rises (B3). The better the cross-functional cooperation, the lower the risk that any one department will focus on local goals at the expense of the larger system. In the case of salespeople, they must become aware of the impact that sales discounts have on company profit. Having a better understanding of how the whole company functions and how it generates profit leads to a more judicious use of discounts and less undermining of the company’s revenue.

This change in behavior needs to be supported by incentive systems. Simply establishing stretch sales goals initiates the B1/R2 loops all over again. And with whom do the sales people compete in a system in which they are engaged at increasing the company profit and not just achieving their sales targets? The feeling that “I am a member of the whole company, not only of one department” can lead salespeople to compete to eliminate conflicts between departments, unnecessary costs, and customers’ complaints.